Last week we published our updated Long term oil demand outlook, here we explore a key regional demand theme.

Parts of the Middle East are in the early stages of an energy transition, with upstream strategy and capital increasingly oriented towards natural gas. This is being matched by investment in gas-fired power generation, alongside a growing pipeline of utility scale solar projects. Strong solar resource, combined with low cost photovoltaic modules (notably from China), is improving project economics and expanding the range of developments that may proceed.

This shift raises a central question for the power sector: how quickly could legacy oil-fired generation be displaced?

Across the Middle East (including Egypt), oil-fired power plants are estimated to underpin approximately 2 million bpd of liquids demand. In principle, as gas availability expands and solar penetration rises, oil may be reprioritised towards export markets, where it can realise higher value than domestic combustion for power. However, the pace of decline in oil burn may be slower than implied by the most optimistic planning assumptions, for several reasons:

Delivery risk and system constraints. Large infrastructure programmes are frequently subject to delays. The breadth of activity associated with Saudi Vision 2030 may intensify constraints across construction supply chains, labour availability and grid build out. This could slow the commissioning of replacement capacity and, in turn, the retirement of oil-fired generation.

Power system balancing may remain thermal led. While battery storage is increasingly deployed elsewhere to manage intermittency from solar generation, the region may continue to rely on thermal flexibility – primarily gas-fired power plants – as the main balancing mechanism. Where oil-fired units continue to provide dispatchable capacity and reserve margin, the case for rapid retirement may be weaker.

Load growth may absorb additional low cost supply. Over the forecast horizon, incremental electricity supply may be partially absorbed by higher cooling demand, industrial expansion, data centre growth and other electrified end uses. Electric vehicle adoption may also rise in parts of the region. In this context, a slower retirement of oil-fired units – aligned with technical life and reliability requirements – may persist even where export economics are favourable.

Regional demand and interconnection may support utilisation. While much of the near-term investment is concentrated in the GCC core, latent demand in neighbouring markets remains significant. The build-out of regional interconnectors may result in a greater share of load growth outside the core being met through cross border supply and system balancing. This could support higher utilisation of the wider thermal fleet over the transition.

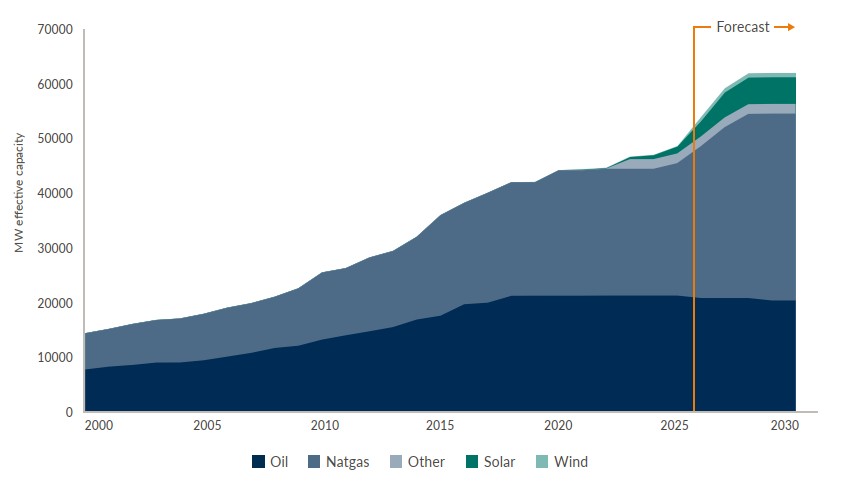

Saudi Arabia Powergen, Effective Capacity

On balance, oil-fired generation may be materially, but not fully, displaced by 2040. In our outlook, regional power sector liquids demand may decline to around 1 million bpd by 2040, with limited crude burn remaining and a modestly higher share of ethane and LPGs within the residual liquids slate.

Visit vitoloutlook.com for more on our long term oil demand outlook.