Road vehicles are the single biggest consumer of oil, accounting for around half of all oil use at approximately 50m b/d, and contributing almost 20% of global CO2 emissions.

With population growth and economic expansion set to drive transport demand even higher in the coming years, a shift away from the internal combustion engine (ICE) is critical to a more sustainable transport solution.

Transitioning to low-carbon propulsion is underway in many developed economies and set to surge in the coming years. Vitol expects electric vehicles (EVs) will comprise around 17% of global car sales by 2025 (almost double from last year), 40% by 2030, and over 80% by 2040, displacing more than 12m b/d of oil demand.

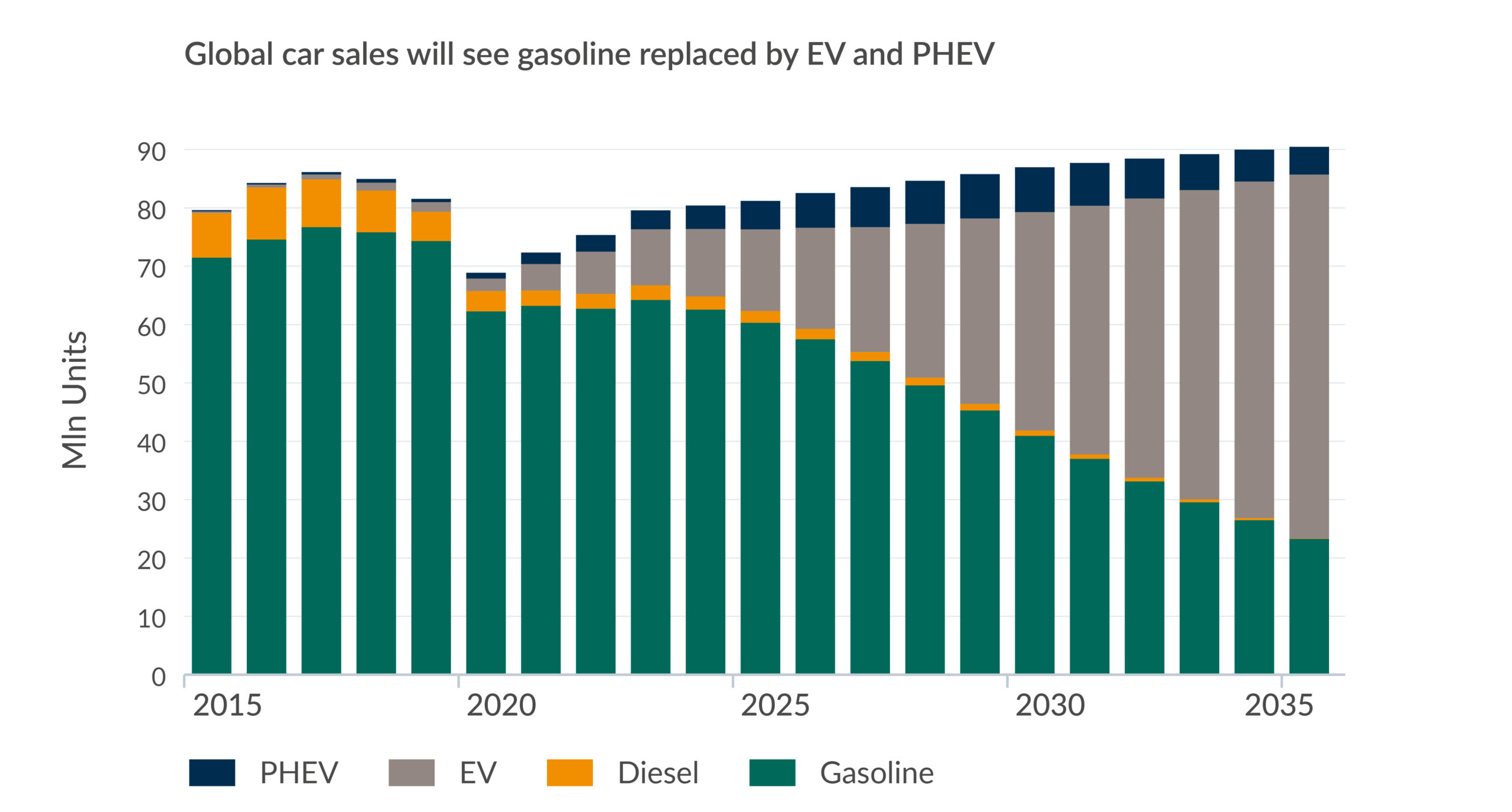

It’s worth noting that Vitol anticipates annual global car sales to rise through the 2020s and 30s, nearing 90 million units by 2035. The key differentiator is the increasing dominance of battery EVs (BEV) and plug-in hybrid EVs (PHEVs). New registration of gasoline cars will drop from 81% in 2023 to 26% in 2035, with diesel engines all but eradicated.

Global BEV sales generally outperformed industry expectations last year, accounting for around 1 in 8 new cars sold in 2023. This represents a year-on-year gain of almost a third, with China remaining the largest EV market (20% market share). Increase in model range and availability, as well as lower unit prices this year has driven recent EV growth.

Regional disparity

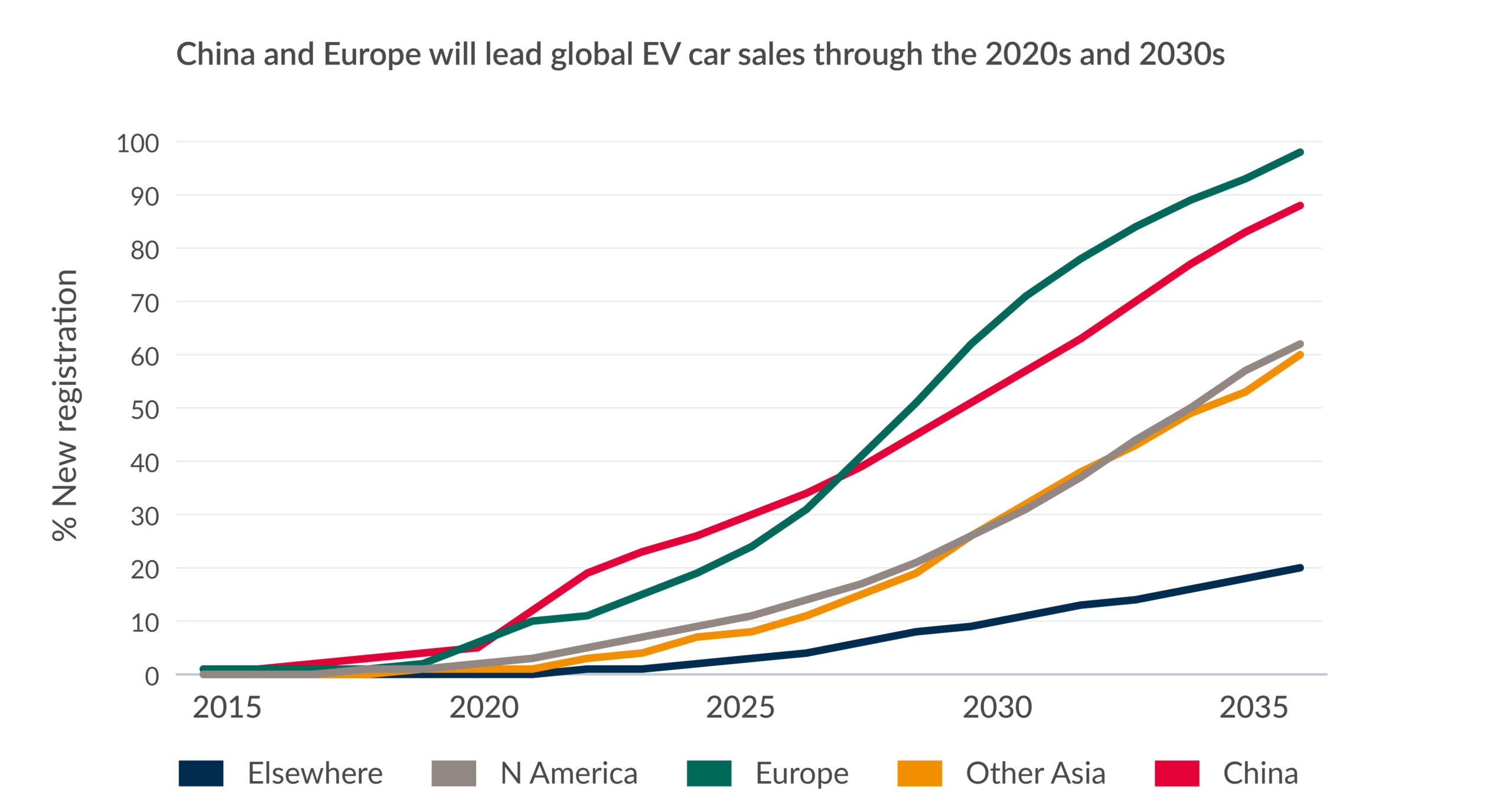

Leading this EV evolution will be Europe and China, with an EV market share of new car sales forecast at 90% and 80%, respectively by 2035. The US by contrast is forecast to have more than 50% market share over the same period. There are several factors for the disparity in EV uptake. China has a younger car fleet, due to relatively recent urbanisation and economic growth, and the average distances travelled is – similar to Europe – much shorter than those seen in the US.

The gasoline vehicle is also more connected to national identify and class mobility in US society than both China and Europe. However, the most important factor guiding regional disparity is the scope and scale of individual region’s regulatory environments, with China leading the way with a consistent policy platform since 2009.

Strengthening policy

China’s government has for several years implemented a series of incentives, notably in the form of purchase subsidies and tax reductions. More recently the EU, under its ‘Fit for 55’ package – which aims to cut GHG emissions by 55% by 2030 – will ban the sale of new petrol and diesel cars by 2035. However, e-fuels will be allowed under the new package.

The US will be buoyed by the Inflation Reduction Act (IRA), which will bring billions of dollars of investment to transitional energy solutions over the next decade. By far the biggest consumer of gasoline globally, it’s important that the US transitions successfully to zero emission vehicles. The average American used around 1,400 litres per capita of gasoline in 2022. The second-largest was Canada with just under 1,100 litres. By comparison, China’s equivalent was 120 litres, and proportionally Europe’s biggest consumer – Switzerland – used just 300 litres per person.

In the US, California’s Advanced Clean Cars II regulations have been taken up by several states, including Massachusetts, New York, Oregon and Washington. This will require all new light vehicles sold in the state by 2035 to be either EV or PHEV.

Earlier this year, Joe Biden’s administration announced a new Charging and Fuelling Infrastructure grant programme, created by the Bipartisan Infrastructure Law, as part of efforts to open 500,000 new EV charging stations.

New policies are also targeting EV supply chains. The EU’s Net Zero Industry Act, which was proposed in March this year, aims for nearly 90% of domestic annual battery demand to be met by EU battery manufacturers, with a capacity of at least 550 GWh in 2030. India is looking to boost domestic manufacturing of EVs and batteries through Production Linked Incentive (PLI) schemes. Similarly, the IRA emphasises the strengthening of domestic supply chains for EVs, batteries and battery minerals, in its criteria to qualify for clean vehicle tax credits.

A complicated picture

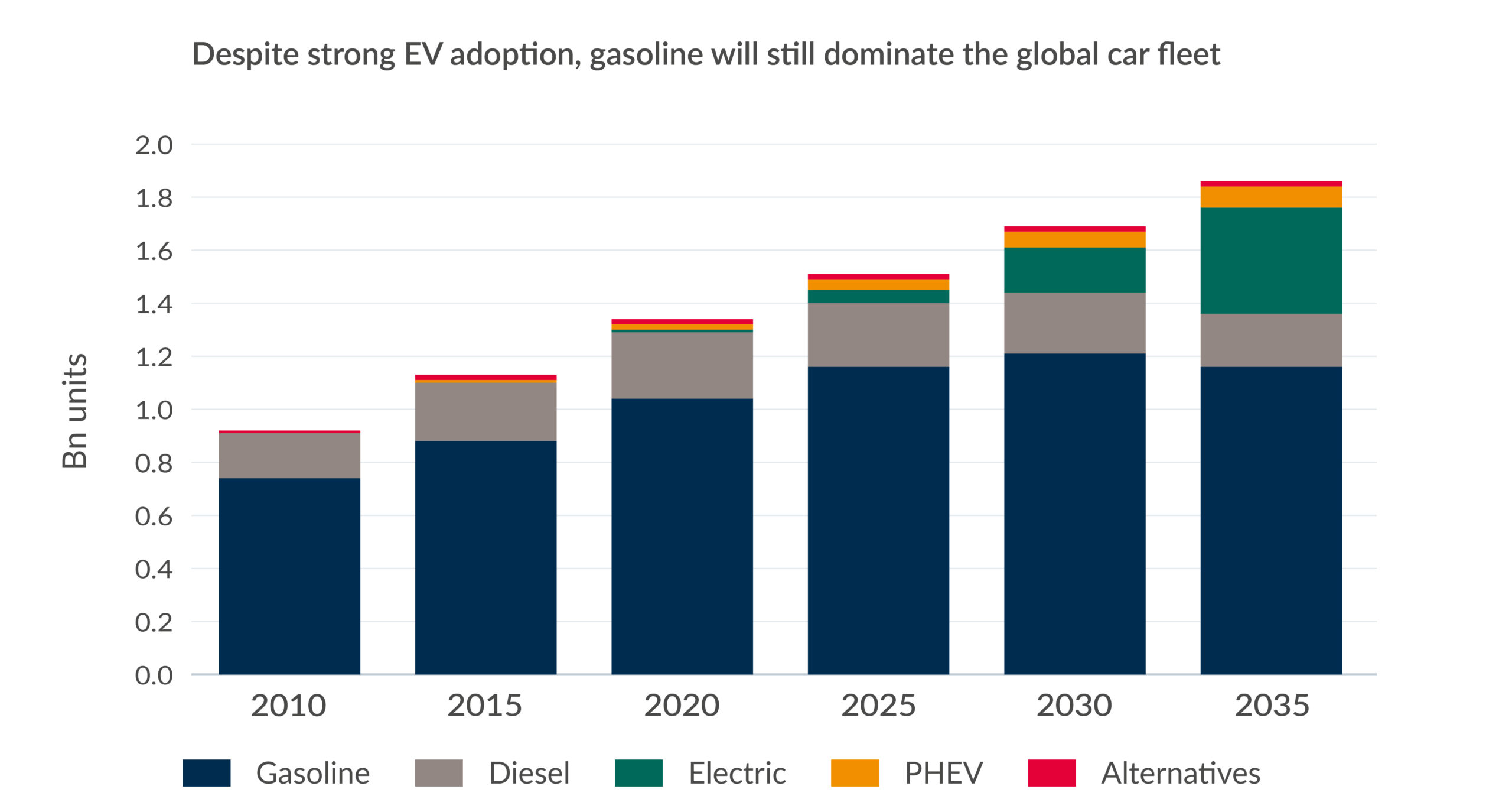

Whilst we anticipate the trajectory of EV vehicles to steadily rise, Vitol expects gasoline to continue to dominate the global car fleet in the coming decade – PHEV’s are essentially a more efficient gasoline vehicle – with ICE units totalling more than 1 billion in 2035, on par with 2025, and EVs only making up one-third of the fleet.

The bulk of these vehicles will be located in less developed economies, where GDP and population growth are surging. As a result, dependence on cheaper, established ICE vehicles will be maintained, hindering efforts for these nations to align with net zero strategies. The longer lifecycle of an ICE vehicle also stifles any concerted shift. Vitol sees low-income fleet ownership to double from around 100 million by 2035.

To offset this, fleet penetration rates could be boosted further by ICE scrappage schemes and usage restrictions. The IEA also calls for better planning policy for compact urban development with improved public transport and infrastructure for micro mobility.

There are also complementary strategies to electrification that will aid the reduction of carbon emissions from the car sector. This includes low-carbon fuels such as hydrogen or biofuel, increasing energy efficiency, as well as a structural shift in passenger use like encouraging shared mobility.

Unlike passenger and light commercial vehicles, decarbonising heavier vehicles poses a different set of challenges that will require a different set of solutions. All the concerns that were laid at cars for EVs – charging infrastructure, range anxiety and cost – are magnified with trucks, given the heavier nature of vehicles and typically longer journeys.

Vitol will explore these challenges and possible solutions, including biofuels and hydrogen fuel cells in a future article.